JANA BUDKOVSKAJA: Estonian angels have grown up. Now the government needs to catch up.

Jana asks the Estonian government: "Please put five million on the table" for an angel co-investment vehicle. She promises extremely positive development in 3 years.

EstBAN's five-year data tells a story of maturation, but without a co-investment instrument, the smartest investors in the ecosystem will keep sitting on the sidelines.

Every year, the Estonian Business Angels Network surveys its members about what they invested, where, how much, and what they plan to do next. Spending some time inside this data, I found a story that is more nuanced, and more urgent, than a simple graph with declining numbers.

Angel investment volumes are down, but when you look across five years of data and correlate it with the broader Estonian startup ecosystem, the picture emerges. This is a maturation, one that comes with a very specific warning for policymakers and a very clear opportunity window that will not stay open forever. Let me walk you through the numbers.

The big picture: capital is shrinking, but the system is changing

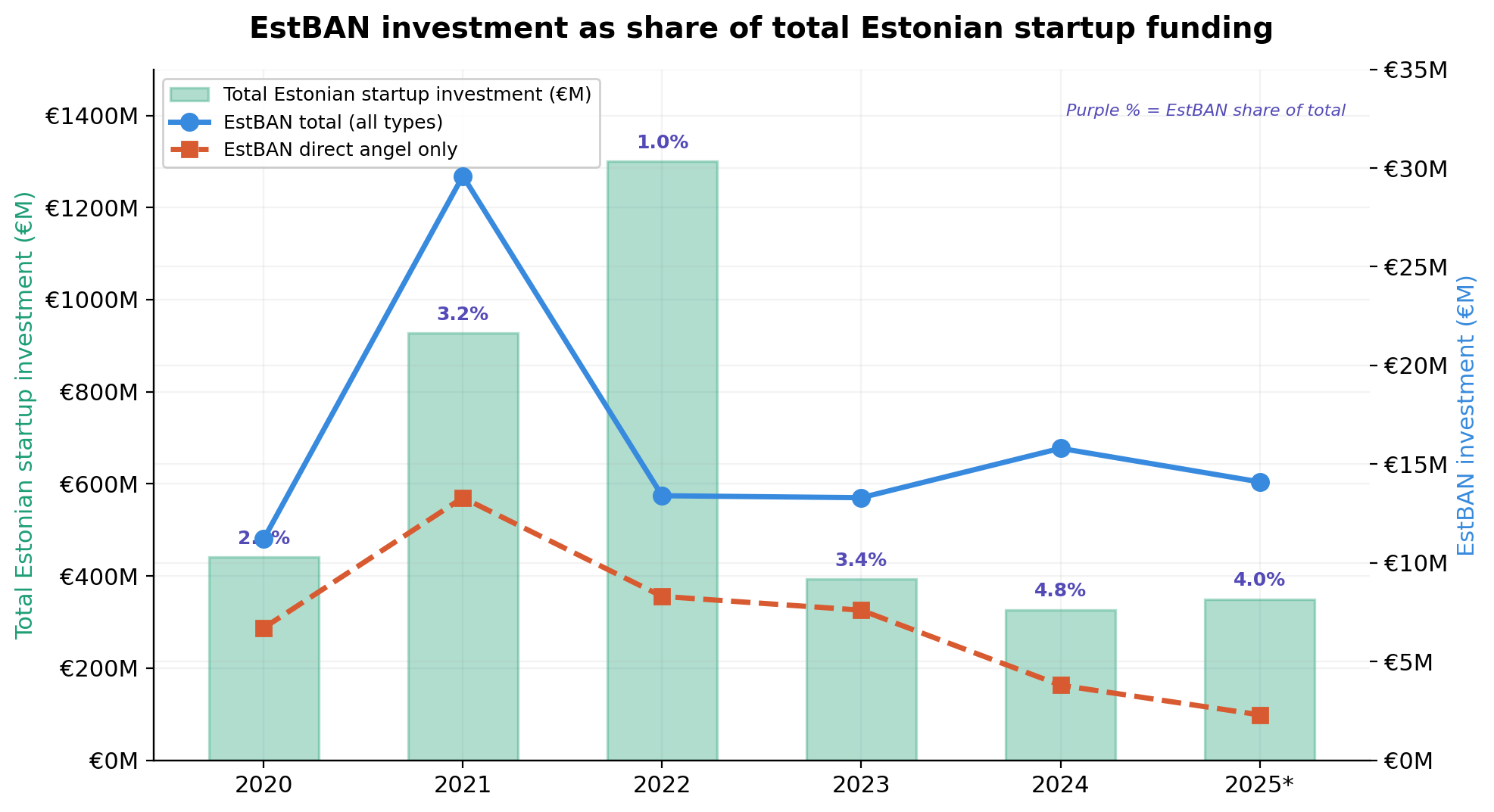

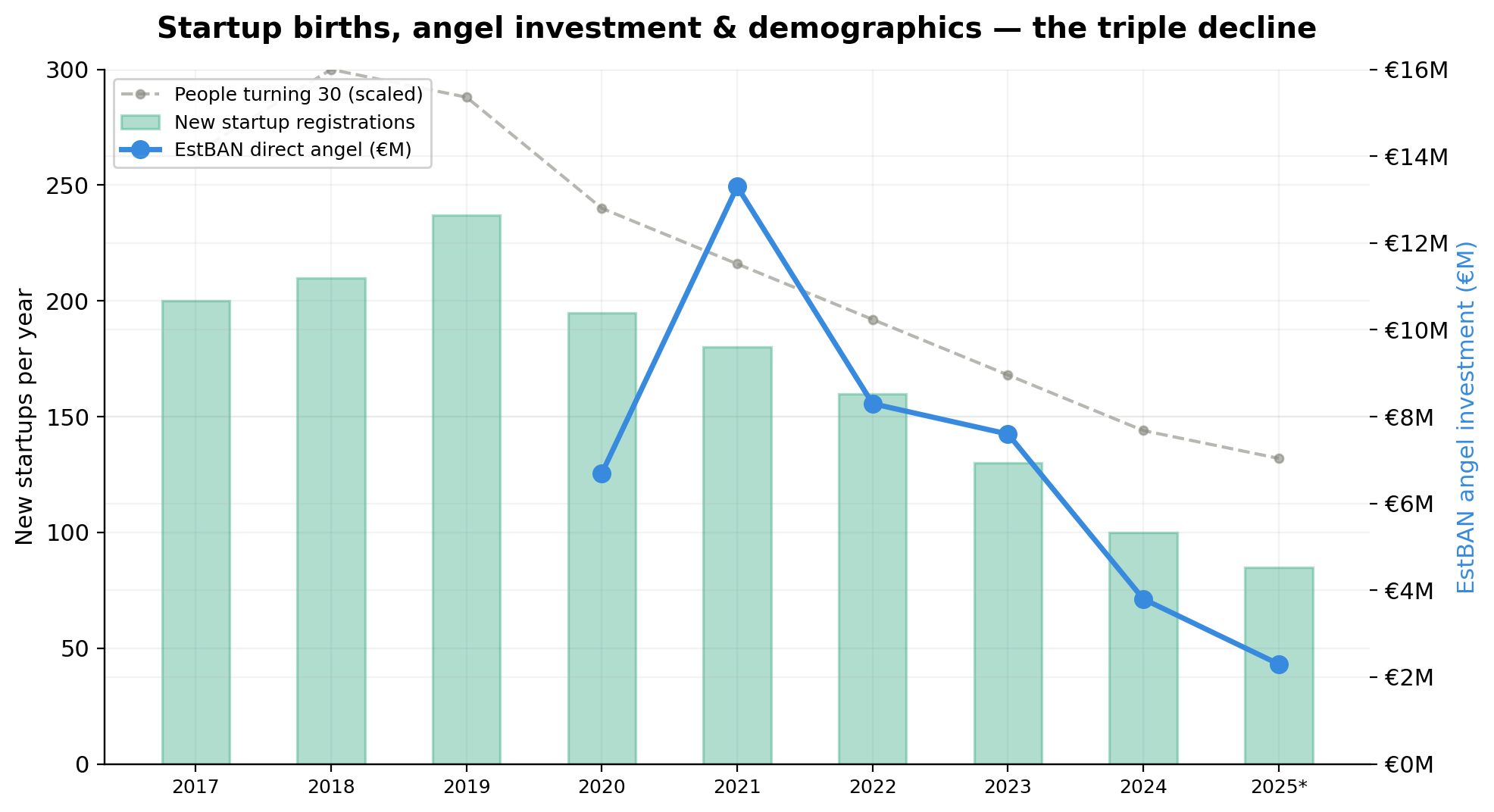

EstBAN members deployed €14.1 million into startups in 2025. That sounds respectable until you learn that direct angel investment, the real first-cheque capital, where an investor writes a personal cheque into a founder's company, fell to just €2.3 million. Four years ago, that number was €13.3 million. That is an 83% drop. But it's not the drop of investments, it's the drop of 'how' the money was invested.

Meanwhile, fund investments by the same community rose to €11.8 million. Our angels have not stopped investing. They have shifted how they invest, moving from direct deals into managed vehicles, from solo bets into structured funds.

This is what maturation looks like. In the early 2020s, everyone was over-excited. The geopolitical situation and the market played their game, and now we are where we are. We have survived the biggest downshift in startup investments after 2022. We are in a post-correction period. The question is not what happened but what we have learnt and what road we take next?

Angels are the canary in the coal mine

Here is the correlation that should keep every institutional investor and policymaker in this country awake at night.

When you overlay EstBAN's direct angel investment onto the total Estonian startup investment data — the €441 million in 2020, the €928 million in 2021, the €1.3 billion peak in 2022, and the decline to roughly €327 million in 2024 — you see something remarkable: angels are basically forecasting what will happen in the institutional market one to two years later.

Direct angel investments and EstBAN's total deployment grew rapidly from 2020 to 2021, then institutional capital followed with its enormous 2022 peak. When angel investment started declining in 2022, institutional capital followed down in 2023 and 2024.

What does the 2025 angel data tell us? It is still declining. This is a red flag for the next stage of investments: if no one is backing and nurturing the earliest companies today, institutional investors will not have enough quality deal flow tomorrow.

We are not just watching a trailing indicator. We are watching a leading one.

Smaller cheques, smarter angels

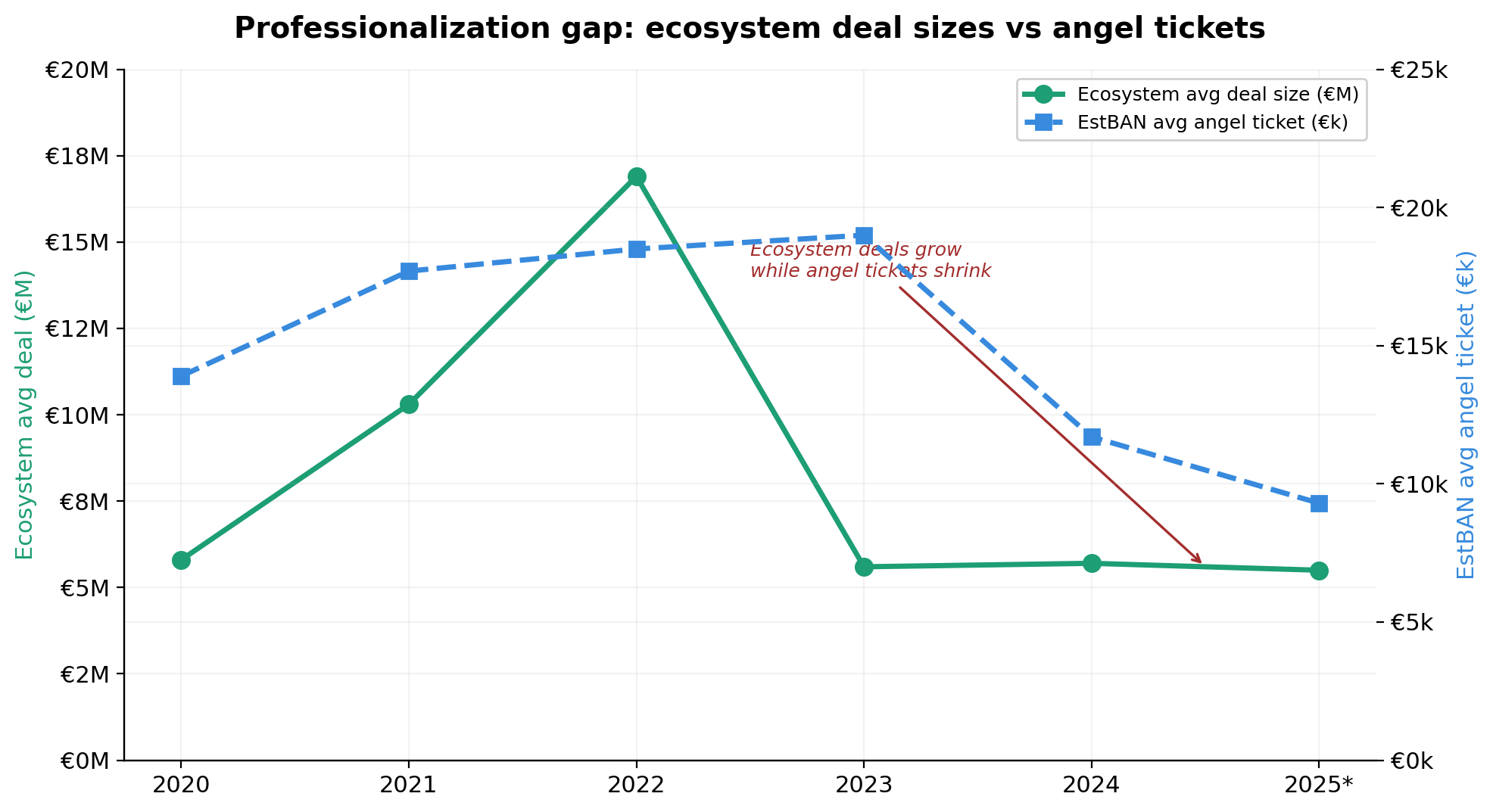

Another trend that might look alarming on the surface is actually a sign of sophistication. The average angel ticket has declined from around €18,500 per investment in 2022 to roughly €9,300 in 2025. At the same time, ecosystem-level deal sizes have stayed in the millions.

It means that our business angels are building portfolios. They understand that to manage risk, you diversify. You write smaller cheques across more deals rather than concentrating on fewer bets. This is an early-stage portfolio strategy, and the fact that Estonian angels are doing it instinctively speaks to the quality of this investor community.

That said, the shrinking of cheques has its limitations. There is a floor below which an angel investment loses its meaning. We may be approaching it.

DeepTech and defence: the momentum we must not waste

What I cannot hide is my personal excitement about where our angels are choosing to invest.

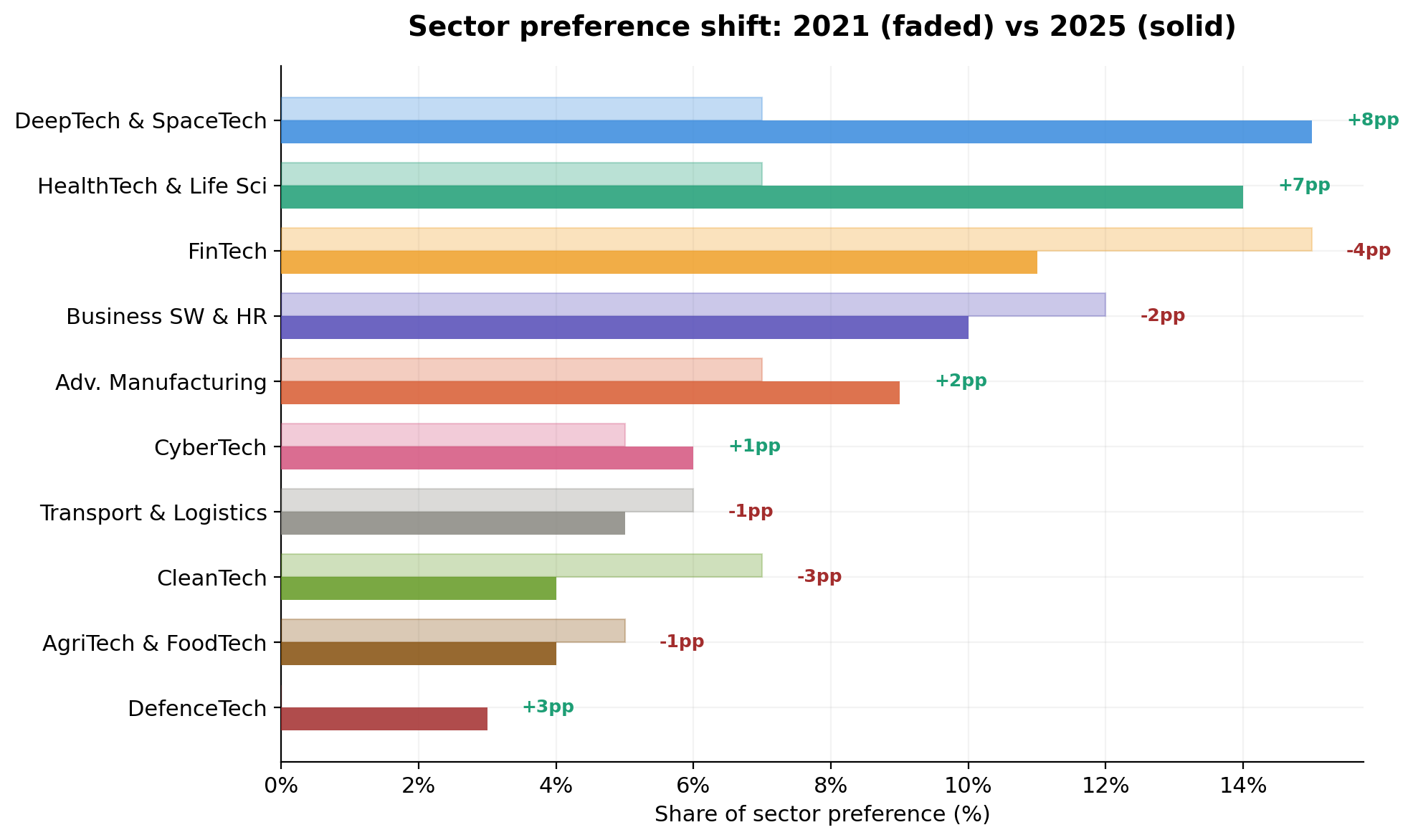

DeepTech and SpaceTech climbed from 7% of sector preference in 2021 to 15% in 2025, making it the number one sector for EstBAN investors. HealthTech and Life Sciences rose to 14%. DefenceTech appeared on the map for the first time at 3%.

As someone who comes from the cleantech world of Beamline and now works across deeptech and defence innovation in BSV Ventures, I cannot be more energised by this shift. Some of it, yes, I may have influenced as one of the lead investors in several syndicate deals last year. But the broader signal is clear: the trust of EstBAN members towards DeepTech is growing, and this is the momentum we need to use.

In Lithuania, as soon as co-investment and profit-share instruments appeared, they saw the same shift. Business angels turned towards DeepTech and defence because they could see clear opportunities and share the risk with the state.

Estonian angels have arrived at this point on their own. Now the question is whether the system around them will grow up too.

The pipeline is narrowing and demographics will not save us

There is another correlation in this data that deserves attention. New startup registrations in Estonia peaked around 237 per year in 2019. By 2024, that number had fallen to roughly 100. A 64% decline.

This tracks almost perfectly with the decline in angel investment and deal count. And it tracks with demographics — the number of Estonians turning 30, historically the peak startup-founding age (as we learned from a historical presentation by Allan Martison), has fallen by roughly 40% since 2018.

Fewer founders means fewer companies to invest in. Fewer investable companies means less angel activity. Less angel activity means less deal flow for institutional investors two years later. It is a reinforcing cycle.

This is exactly why the government's new programme to develop more spin-offs from universities, launched in January this year with the goal of creating several dozen DeepTech startups, matters so much. But those startups will need first-check capital and experienced business people on board. And right now, these resources are drying up.

A misleading number of 32% invested zero

Let me address something that could easily become a misleading headline: 32% of EstBAN survey respondents deployed zero capital into startups in 2025.

I do not want to dramatise this, it is absolutely normal, in more established BANs only 15-30% of members are actively investing every year. Business angels in Estonia invest from their own pocket, without any taxation preferences, without co-investment systems, into the riskiest asset class that exists. In challenging times, sitting on the sidelines is not a failure of nerves. It is smart risk management.

I am very proud that in crisis times, our angels are thoughtful. The ones who are investing are writing more diversified, more strategic cheques. The ones who are not investing are waiting for better conditions. Both behaviours are rational.

But here is where policy comes in: if you want those rational, experienced, well-networked investors to come back off the sidelines, you need to change the risk-reward equation.

The case for a co-investment system: €5 million to turn the trend

In Finland, they have a co-investment system and in Lithuania, they have a co-investment system plus a profit-share mechanism. Both countries have seen measurable increases in angel investment activity after introducing these instruments. Estonia has neither.

We rank number one globally on the Tax Foundation's International Tax Competitiveness Index, for the twelfth consecutive year. We have one of the most digital, efficient business environments in the world. And yet we are one of the only competitive startup ecosystems in Europe with zero angel-specific investment incentives.

The numbers make the case themselves. EstBAN's direct angel investment was €2.3 million in 2025. A 1:1 government co-investment match at the syndicate level would double that to €4.6 million, and the additional deal flow, confidence, and network effects would likely push it even further. Given the scale, we could start with just €1 million per year and already create a meaningful impact.

My ask is simple: Estonian government, please put five million on the table. In three years, you will see extremely positive trends.

If we start a co-investment system next year, we can turn the declining trend by 2028, reaching back to 2022 levels of angel activity. By 2030, we can aim for 2021 levels. And as we have seen from the data, when angel investment turns positive, institutional investment follows.

From regression to progression

We are not in a crisis. We are at a crossroads. Estonian business angels have matured from enthusiastic first-timers into sophisticated portfolio builders. They have shifted towards DeepTech and defence — exactly the sectors where Estonia has a strategic competitive advantage.

The ecosystem around us is thriving. Baltic startups raised a record €607 million in 2025. Estonian startups generated €1.8 billion in added value, contributing 4.3% of GDP. Foreign funds are actively looking for opportunities here.

But there is a gap forming at the earliest stage – the first cheque, the pre-seed, the moment when a founder needs not just money but a business angel who has been through the growth journey, who brings networks, who brings operating experience. That is the stage where the university spin-off meets the experienced entrepreneurs and gets a valuable network. Where different competences and experiences come together – the business magic happens.

That stage cannot be funded by institutional capital. It needs angels. And right now, the angels need a signal from the system that their risk-taking is valued.

A co-investment instrument is that signal. It is not a subsidy, it is a multiplier. For every euro of public money, you unlock more private capital, private networks, and private expertise that no public programme can replicate.

The data is clear. The opportunity is clear. The next move belongs to the policymakers.

Jana Budkovskaja is a member of the management board of the Estonian Business Angels Network (EstBAN) and Partner of BSV Ventures. She has supported investments in more than 100 teams. In 2025, she co-led EstBAN syndicate investments at Startup Day and Latitude59. The analysis in this article is based on EstBAN's annual survey data from 2020–2025, Startup Estonia ecosystem reporting, the Baltic Startup Funding Report 2025 and photos of presentation by Allan Martinson.