ALEJANDRO JIMENEZ: Optimising balance sheet

Why Apple & wealthy individuals use both equity & debt

Striking the right balance between equity and debt can optimise your company’s balance sheet and fuel its growth. Every business requires equity, while debt is mostly optional.

Borrowing money can complement equity and boost returns, without diluting ownership. The key behaviour is to borrow responsibly.

Major corporations and wealthy individuals borrow frequently

Apple owes $83 billion in debt, with repayment dates ranging from immediate to 30+ years. More eye-popping is that its operating profits were $87 billion in just the last six months, implying it could repay all its debt with incoming cash flow in under a year (not to mention the $68 billion it holds in cash and liquid securities).

When I managed investment portfolios for wealthy individuals, many of them billionaires, they also borrowed often despite already having enormous amounts of money.

Why would Apple and billionaires borrow? In simple terms, because their return on assets is usually greater than their cost of debt, thereby capturing an excess return with borrowed capital, without needing to divest existing assets. They strategically manage their assets, debt, and equity to optimise returns.

Apple believes it can reinvest its debt at a return greater than its average interest cost of 3-4%. Examples of such investments include research and development in AI, the creation of new products like smart glasses, the acquisition of startups, tax optimisation, and buying back its own equity to increase its stock price (fewer shares in the market mean each remaining share is worth more).

Wealthy investors take a similar approach when needing fresh capital. Rather than liquidating existing profitable assets, they’ll borrow to pursue new opportunities, such as investing in their operating company, buying stocks and bonds, acquiring private companies, and purchasing sports teams.

What is a healthy amount of debt?

For companies, three metrics are generally monitored to assess “debt healthiness”: debt-to-operating profits, interest coverage, and debt-to-equity.

Debt-to-operating profits ratio: A healthy amount is generally when a company’s total debt balance is 1-4x its annual operating profits. In other words, it would take 1-4 years of profits to fully pay down the debt principal.

Interest coverage ratio: A ratio over 2x is generally healthy. This measures a company's capacity to pay interest, indicating how many times annual operating profits exceed annual interest costs.

Debt-to-equity: A healthy ratio is typically a maximum of 40% debt and a minimum of 60% equity, indicating the funding mix between borrowed money and owner investment. It’s the company's "equity cushion" to absorb operating losses.

For individuals, measurements vary based on the type of asset purchased with debt. When buying a home, the standard is 80% debt vs 20% equity. However, always ensure your recurring income is enough to comfortably meet ongoing loan payments.

When investing in assets like stocks, bonds, or private companies, my former clients would generally borrow a healthy 20-25% of the total value of their portfolios. Riskier ones would go up to 30-35%.

Be careful if you’re borrowing to spend rather than to invest. Have a plan for how you’ll eventually repay that loan if there’s no asset behind it that produces returns.

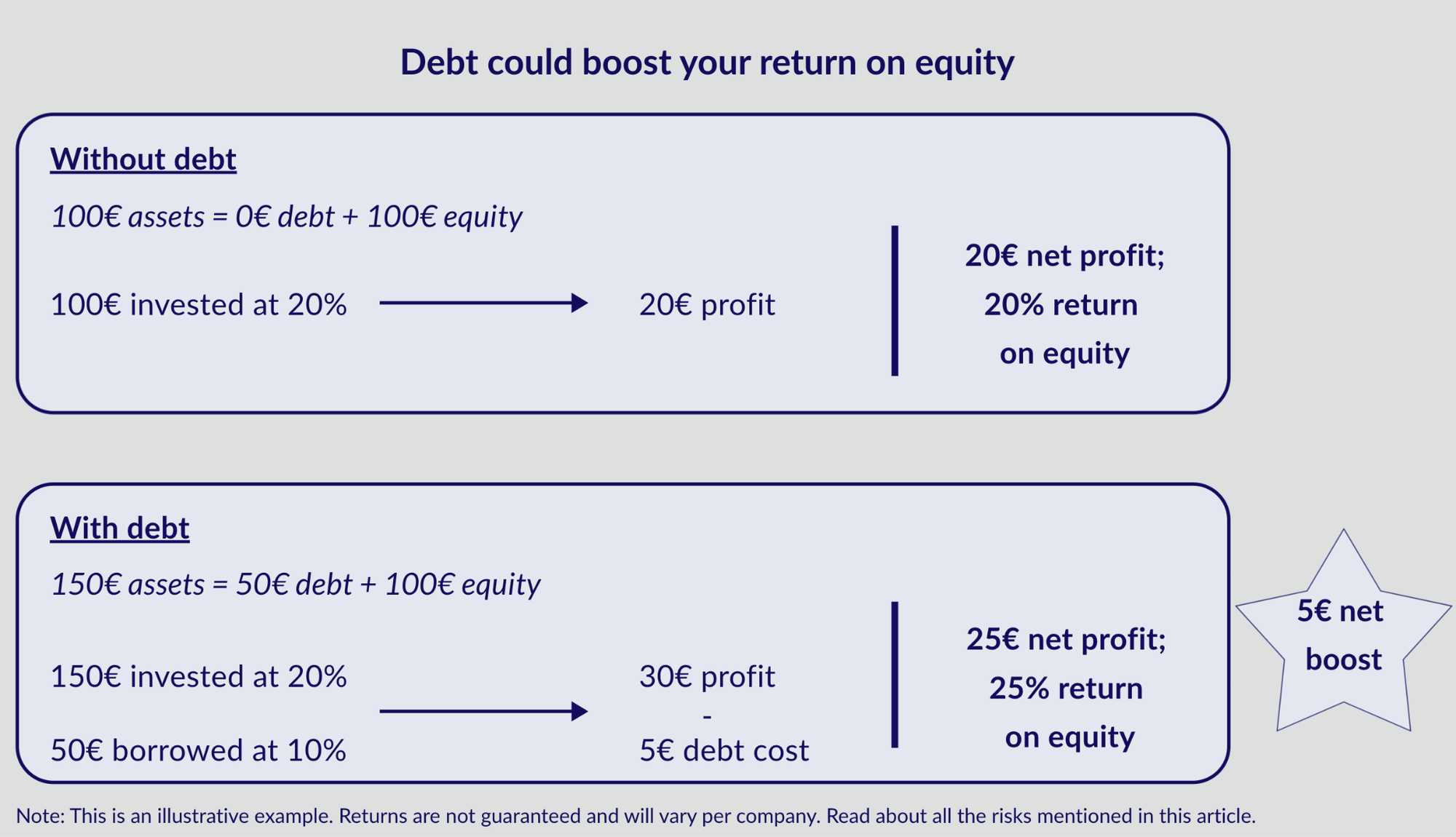

Borrowing could increase your return on equity

Let’s do a simple example with round numbers.

Imagine you own a small company with 100€ in assets generating annual profits of 20€. You have no debt, so your equity (ownership) is the full 100€. Your return on equity is therefore 20%.

You wish to expand your company’s capacity by 50%, which would require an investment of 50€, and you believe it can sustain the same level of profitability. However, you don’t want to raise equity because this means selling ownership.

Instead, your company borrows 50€ at an annual interest rate of 10%.

Now the company operates with 150€ in assets, 50€ in debt, and 100€ in equity, boosting profits to 25€ (up from the previous 20€).

Your return on equity rises to 25%, up from 20%, making your company more valuable.

Of course, your company will eventually have to pay back the 50€. The risk is that if the expansion project fails, the company would need to sell assets to cover the loan. If the assets are sold at a low value, it may eat into your equity.

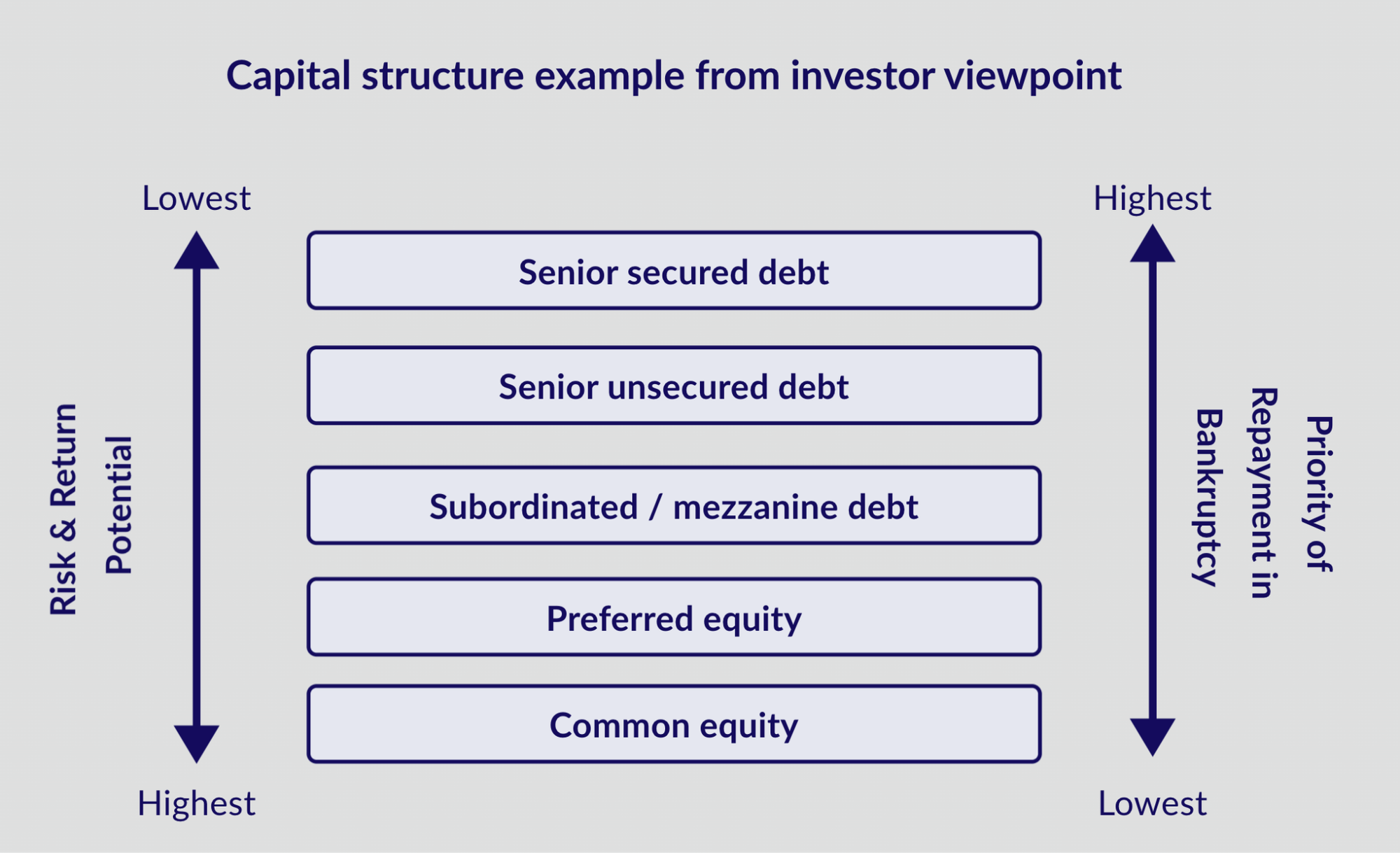

Capital structure is the mix of debt and equity on a company’s balance sheet

When raising capital for your company, always remember that investors see through a risk-versus-return lens. The greater the risk, the higher return they’ll expect.

Equity carries the highest risk for investors, but offers potentially unlimited upside. Debt offers investors a lower return, capped at an interest rate, but better protection via their right to seize company assets in case of bankruptcy.

Startups begin with equity, but scaleups & small businesses can look to debt

Early-stage startups generally don’t have much choice but to raise equity (or convertible debt that converts to equity). The reason is that investors want to maximise their return in exchange for the high risk of investing in such a young company. A loan’s low return doesn’t compensate for the risk investors take at this stage.

Once your company scales and matures a bit, you’ll likely have collateral or cash flow that makes lenders comfortable. At this point, taking a loan benefits your company in that no ownership is given up.

Borrow responsibly

Responsible borrowing means to:

- Plan for multiple scenarios, including a worst-case outcome where the asset purchased with the loan fails;

- Ensure the expected return of the asset is at least 3-4% greater than the cost of the loan, providing a cushion for unexpected events;

- Match the currency of the asset with that of the loan to eliminate foreign exchange risk;

- Pair the loan’s duration with the productive life of the asset to match cash flows;

- Structure a mix of floating and fixed-rate loans to hedge against unfavourable movements in interest rates;

- Research tax benefits or consequences in your operating jurisdiction;

- Keep liquidity buffers to cover several months of debt payments;

- Maintain a healthy amount of debt vis-à-vis cash flow and equity.

P.S. If you need advice on balance sheet optimisation, reach out to me. At TriHeritage, we’re happy to offer advisory services to help you plan a strategy.

----------------

Alejandro Jimenez is Co-founder & Managing Partner at TriHeritage Global Capital, an Estonia-based firm providing loans and advisory to small and midsize companies across the EU. Previously, Alejandro was a partner in New York and Geneva at J.P. Morgan, the world’s largest financial institution. He also ran the energy trading desk at Enefit and managed sustainable investment portfolios at Grunfin.

Comments ()